KEYTAKEAWAYS

- Polymarket’s move is less about “leaving Polygon” and more about owning the full stack—product control plus value capture.

- Multiple data points suggest Polymarket may have contributed roughly ~25% of Polygon’s activity in key dimensions (TVL share and gas spend).

- Timing likely ties to an upcoming TGE: migrating before token issuance avoids higher coordination costs and expands the valuation narrative.

CONTENT

Polymarket plans to leave Polygon and launch its own Ethereum Layer 2, POLY. Here’s the product and economic logic, plus how much value Polymarket likely contributed to Polygon.

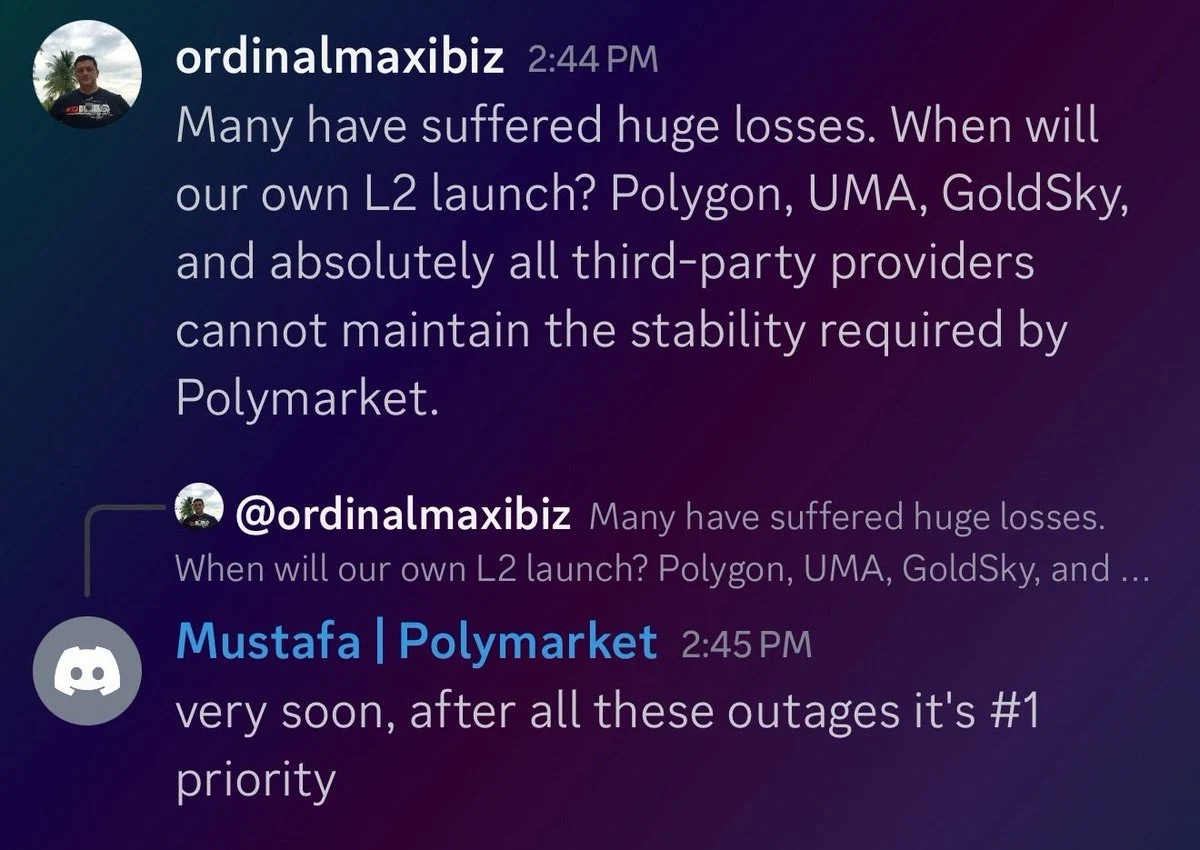

On December 22, an update from leading prediction market Polymarket drew widespread attention across the market. In its Discord community, team member Mustafa confirmed that Polymarket plans to migrate away from Polygon and launch an Ethereum Layer 2 network called POLY—now the project’s top priority.

A BREAKUP THAT WASN’T EXACTLY UNEXPECTED

Polymarket’s decision to move beyond Polygon is hardly surprising. One is a breakout, headline-grabbing application at the forefront of the market; the other is an aging base layer that has been losing momentum. The gap in market attention and value expectations between the two has long felt misaligned. As Polymarket has grown into a new heavyweight, Polygon’s less consistent network performance (with the most recent outage on December 18) and comparatively thinner ecosystem have increasingly become real constraints.

For Polymarket, building its own network is a win-win—both as a product choice and as an economic strategy.

On the product side, beyond simply seeking a more stable operating environment, launching its own Layer 2 allows Polymarket to tailor underlying features around its platform’s specific needs, making future upgrades and iterations far easier to execute.

More importantly, the bigger value lies in the economics. A self-owned network enables Polymarket to internalize the economic activity and surrounding services generated by its platform—preventing value from leaking to external networks and instead steadily compounding into a long-term, system-level advantage.

>>> More to read: What is Polymarket? Web3 Prediction Market

VISIBLE AND HIDDEN ECONOMIC CONTRIBUTIONS

As an application-layer heavyweight, Polymarket’s breakout success delivered clear, direct economic value to Polygon. Historical data compiled by Dune analyst dash shows:

- 419,309 monthly active users; 1,766,193 total users historically

- 19.63 million transactions this month; 115 million total transactions historically

- $1.538 billion in trading volume this month; $14.3 billion in total historical volume

As for how to estimate Polymarket’s share of Polygon’s broader economic activity, Odaily Planet Daily noticed a rather striking “coincidental” ratio when comparing the two ecosystems.

First, in terms of capital retained on-chain: DefiLlama data shows Polymarket’s total open positions across the platform at roughly $326 million, which is about one quarter of Polygon’s total TVL of $1.19 billion.

Second, in terms of gas consumption: Coin Metrics reported in October last year that transactions related to Polymarket were estimated to account for 25% of Polygon’s total gas usage.

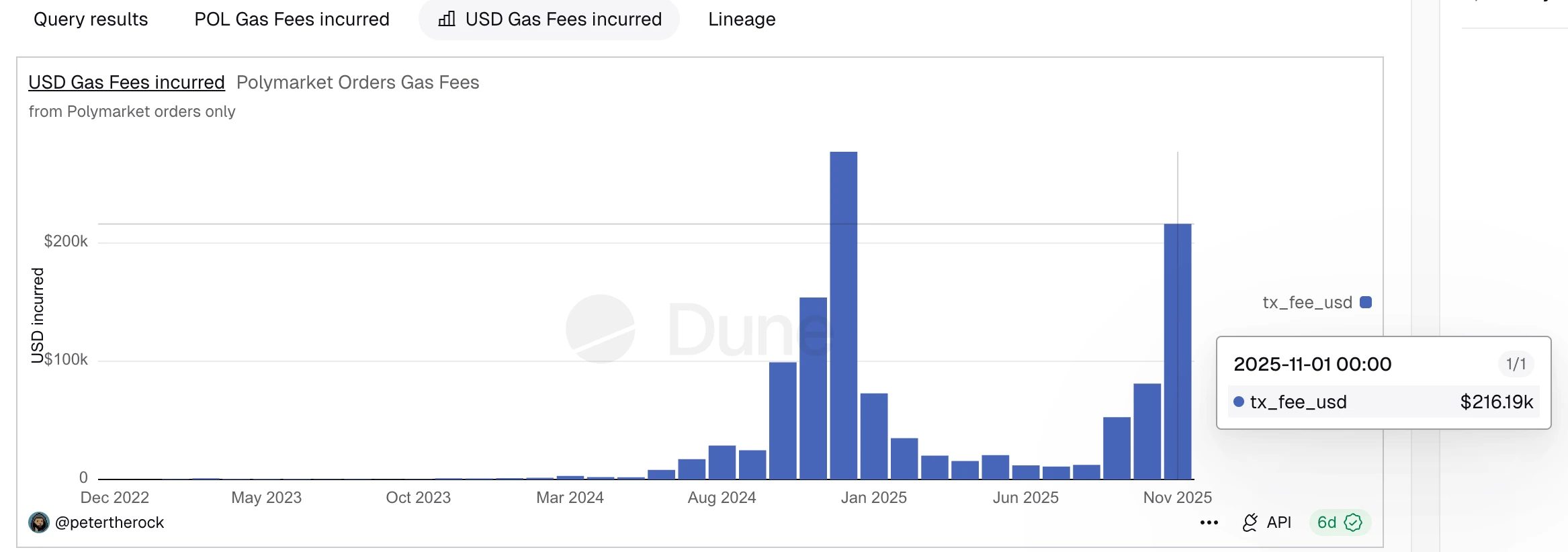

Since that dataset is somewhat dated, we also checked more recent figures. Dune analyst petertherock shows that in November, Polymarket-related transactions consumed roughly $216,000 in gas, while Token Terminal estimates Polygon’s total gas spend for the same month at about $939,000—again, close to one quarter (around 23%).

Of course, this similarity could be partly driven by differences in methodology and time windows. Still, seeing a comparable ratio across multiple dimensions provides a reasonable reference point for approximating Polymarket’s economic significance to Polygon.

Beyond measurable indicators such as active users, retained capital, transaction volume, and gas contribution, Polymarket’s economic significance to Polygon also shows up in a set of “hidden” contributions—harder to quantify, but just as real.

First is its role in activating stablecoin liquidity. Since all Polymarket trades are settled in USDC, the platform’s high-frequency, continuous trading behavior has objectively increased demand for USDC circulation on Polygon and expanded real usage scenarios for the stablecoin on the network.

Second is the spillover value of retained users. Even beyond prediction markets, these users may, for convenience, start using other products in the Polygon ecosystem—such as DeFi—thereby strengthening the network’s overall ecosystem value.

These contributions are difficult to capture with clean, concrete metrics, but they represent exactly the kind of “real demand” that base-layer networks value most—and struggle the most to attract.

>>> More to read: What is POL? Polygon’s Ecosystem Upgrade

WHY NOW? THE ANSWER ISN’T HARD TO GUESS

In reality, based on user scale, performance metrics, and market mindshare alone, Polymarket already has the confidence to stand on its own. This is no longer a question of “whether to leave,” but “when to leave.”

Choosing to begin the migration at this moment likely comes down to the approaching Polymarket TGE. On one hand, once Polymarket issues a token, its governance structure, incentive framework, and economic model tend to become more fixed—making any underlying migration later significantly more costly and complex. On the other hand, evolving from a “single application” into a full-stack system of “application + base layer” implies a shift in valuation logic. Building its own Layer 2 clearly raises the ceiling for Polymarket, both narratively and from a capital-markets perspective.

Ultimately, Polymarket’s departure from Polygon is not merely a straightforward infrastructure move—it’s a snapshot of structural change in the crypto industry. When top-tier applications become capable of independently carrying users, traffic, and economic activity, base-layer networks that fail to provide additional value will inevitably be sidelined.