KEYTAKEAWAYS

- Tether’s USAT is not a simple product extension but a jurisdiction-specific stablecoin designed to operate inside the US regulatory perimeter through Anchorage Digital Bank and institutionally managed reserves.

- By separating USAT from USDT, Tether is attempting to reconcile global stablecoin dominance with domestic compliance, effectively creating parallel dollar instruments optimized for different regulatory environments.

- The move reflects a broader shift in stablecoins from crypto-native infrastructure toward systemically relevant financial instruments whose reserve management, custody, and redemption mechanics increasingly resemble traditional finance.

CONTENT

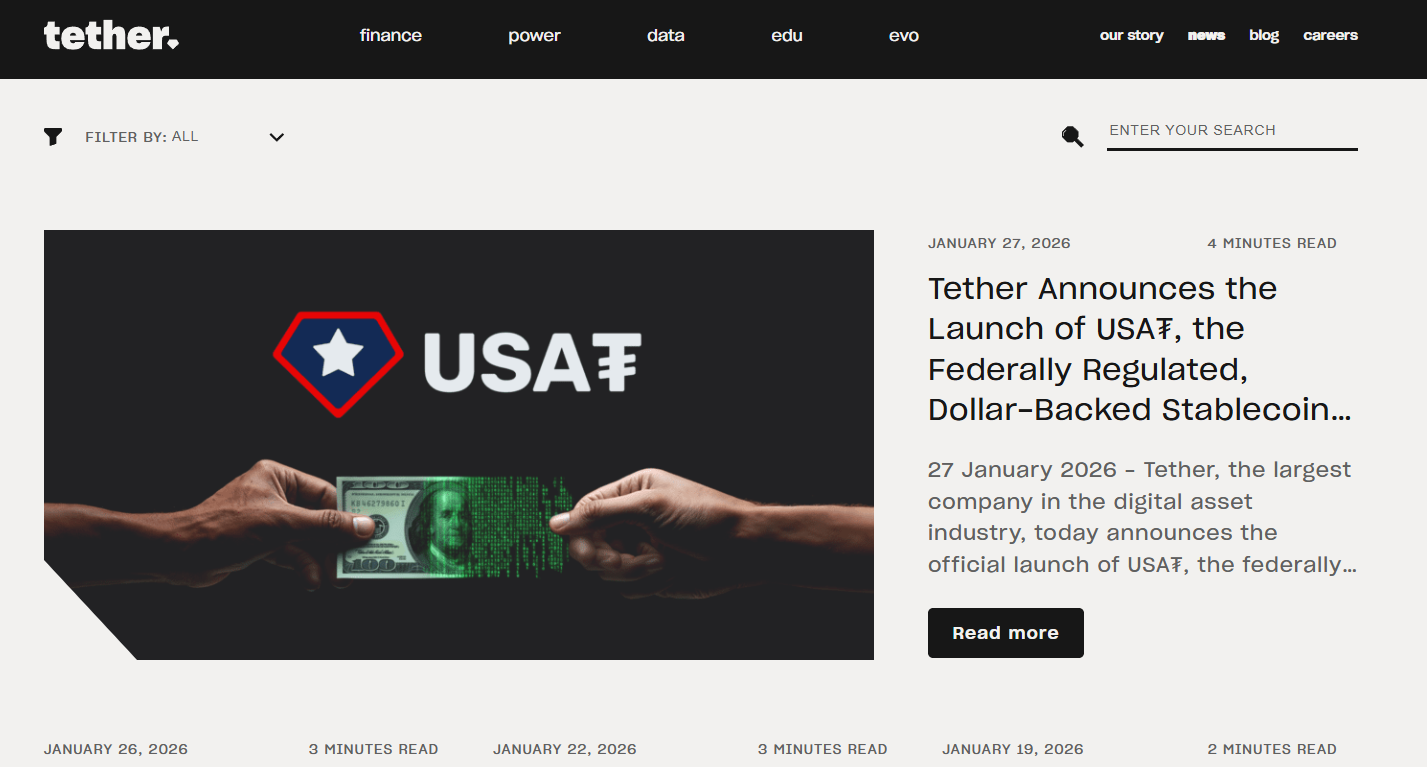

Tether’s launch of the USAT stablecoin signals a structural re-entry into the US market, embedding stablecoin issuance within regulated banking infrastructure while preserving its global USDT liquidity network.

Tether’s “USAT” launch is more than a new ticker—it’s a structural pivot in how the world’s biggest stablecoin issuer is trying to re-enter the U.S. financial perimeter without touching the political and regulatory tripwires that pushed it offshore in the first place. Announced on January 27, 2026, USA₮ (USAT) is positioned as a U.S.-market stablecoin issued inside a federally regulated banking entity—Anchorage Digital Bank—with Cantor Fitzgerald appointed as designated reserve custodian and preferred primary dealer, and with immediate exchange distribution that includes Bybit, Crypto.com, and OKX (among others).

A MADE-IN-AMERICA STABLECOIN, BY DESIGN

For years, the central tension around Tether in U.S. policy circles was not whether stablecoins would win—markets already answered that—but whether the dominant stablecoin issuer could be meaningfully supervised under a U.S. framework while still operating at global scale, and USAT is Tether’s attempt to split that knot by separating product from geography: USDT remains the global workhorse, while USAT is engineered as a domestically aligned instrument whose issuance flows through Anchorage Digital Bank, which Anchorage describes as operating under federal supervision and bank-grade compliance controls, bringing stablecoin minting closer to regulated financial infrastructure rather than leaving it as an offshore-adjacent “crypto plumbing” layer. In practice, that means Tether is not just “listing a new coin,” but inserting a new entity into the stablecoin stack—an issuer with a U.S. charter at the center, reserve oversight delegated to a Wall Street custodian, and distribution routed through U.S.-regulated platforms and banking partners that Tether says are being lined up for broad access.

WHY NOW: A $300B MARKET THAT CAN’T STAY IN LIMBO

Timing matters, because this is happening in a stablecoin market that has quietly become one of crypto’s only truly mainstream rails: on-chain dashboards show roughly $308B in stablecoins outstanding around late January 2026, and USDT dominance around ~60%, which means that even small design changes by the largest issuer can ripple across exchanges, cross-border settlement flows, and DeFi liquidity regimes.

At the same time, the “stablecoin debate” has shifted from philosophical arguments about decentralization toward very old-world concerns—bank disintermediation, deposit flight, and who captures the interest on reserve assets—with major institutions publicly modeling large deposit impacts from stablecoin growth under evolving U.S. rules. In that context, USAT is best read as a political-economy product: it is a way to keep Tether’s liquidity and brand gravity while offering U.S. stakeholders a cleaner story about supervision, reserves, and accountability—especially for institutions that can’t, or won’t, build workflows around an offshore-issued unit of account.

THE RESERVES STORY IS THE PRODUCT

Stablecoins ultimately compete on one thing that sounds boring until it breaks: reserve credibility, and Tether is trying to turn what used to be its greatest friction point into an institutional feature by explicitly naming counterparties and roles. The company says Cantor Fitzgerald will serve as reserve custodian and preferred primary dealer for USAT from day one, which is meant to answer a question U.S. allocators ask immediately: “Who holds the assets, how are they managed, and how fast can redemption stress be met without improvisation?” The move also lands at a moment when Tether’s balance-sheet footprint is increasingly legible in macro terms: Reuters reporting highlights how reserve strategy and non-cash exposures—including meaningful gold positions tied to Tether’s broader reserve behavior—have become large enough to draw comparison to sovereign-scale actors in specific markets, reinforcing the idea that stablecoin issuers are no longer mere crypto intermediaries but shadow monetary institutions whose asset allocation choices matter. In other words, USAT is not simply “USDT, but compliant”; it is Tether acknowledging that in the U.S., the stablecoin product is inseparable from the identity and governance of the reserve machine behind it.

COMPETITION: USDC IS THE TARGET, BUT TRUST IS THE BATTLEFIELD

USAT also reframes the competitive map inside America, where Circle’s USDC historically had the home-field advantage in institutional narratives, while USDT dominated global trading liquidity; by introducing a “U.S.-regulated” sibling product rather than attempting to retrofit USDT, Tether is signaling it wants to compete for the American stack without risking disruption to the offshore liquidity network that made it dominant. But that dual-product strategy introduces a subtler challenge that sophisticated readers will appreciate: fragmentation can become a tax on businesses if multiple “dollars” behave differently across venues, compliance regimes, and redemption channels, and the market will quickly test whether USAT and USDT remain near-perfect substitutes or diverge under stress—through fee tiers, onboarding friction, liquidity depth, and how quickly each instrument can be converted back into bank money at scale. If USAT succeeds, it won’t just be because it exists; it will be because it becomes boringly liquid—deep order books, predictable redemption, and clean integration into U.S. compliance workflows—so that institutions can hold and move dollars on-chain without having to explain to risk committees why their core settlement asset is structurally offshore.

A U.S. RETURN THAT SIGNALS A NEW STABLECOIN REGIME

The deeper takeaway is that Tether’s U.S. re-entry is happening precisely as stablecoins are being pulled into the same gravity well that shaped money markets, prime brokerage, and payment networks: policymakers want stablecoins inside rulebooks, banks worry about deposits and payments, and issuers want the legitimacy that expands distribution. In that world, USAT is a blueprint for how stablecoins may scale in the next phase—not as a single monolithic “internet dollar,” but as a family of dollars optimized for different jurisdictions and counterparties, with reserve and issuance roles increasingly resembling traditional finance, even if the rails remain public blockchains. And because Tether still anchors the majority share of stablecoin liquidity, the success or failure of this design choice will influence whether the U.S. stablecoin market evolves toward consolidation around a few tightly supervised issuers—or toward a more complex landscape where “digital dollars” multiply, specialize, and occasionally collide when liquidity tightens.

Read More:

Tether Adds 27 Tons of Gold in Q4, XAUT Tops 50% Market Share